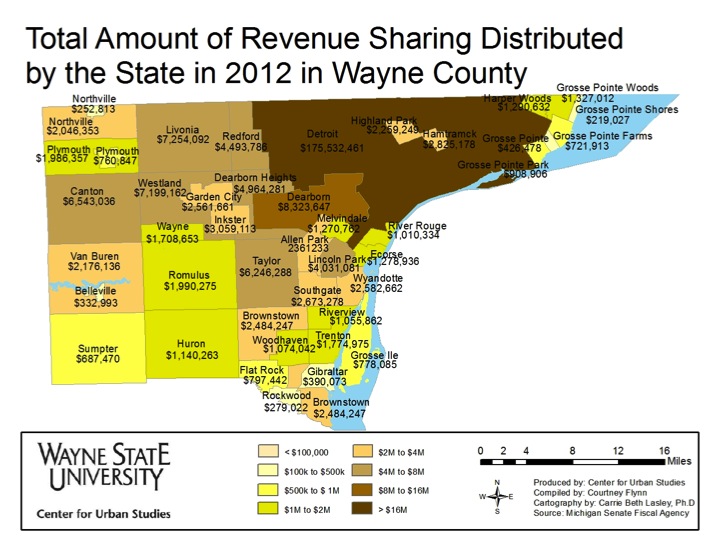

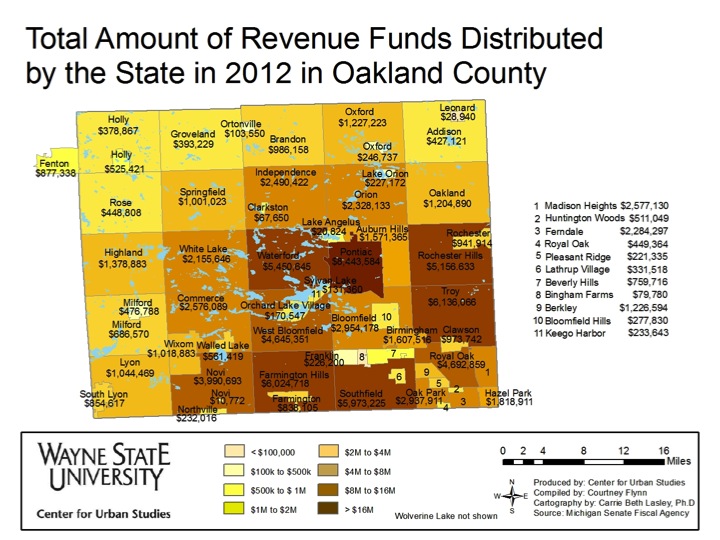

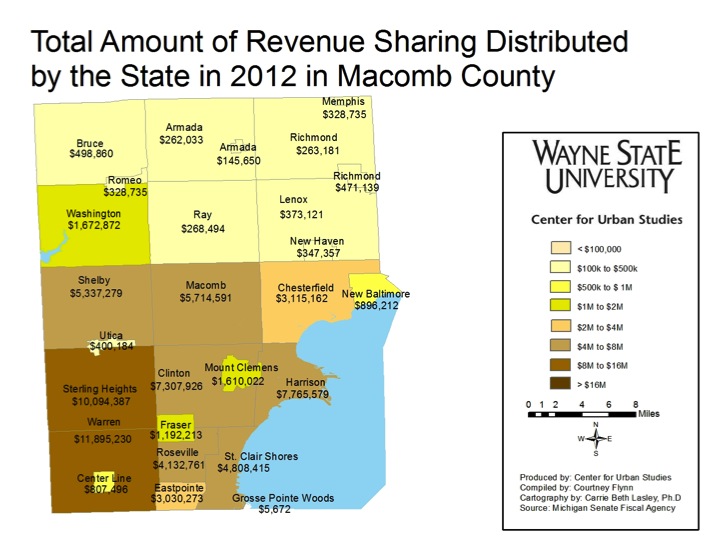

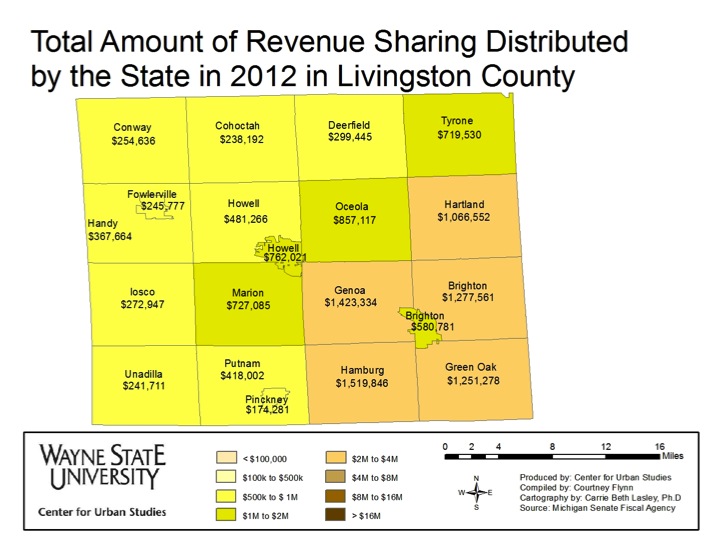

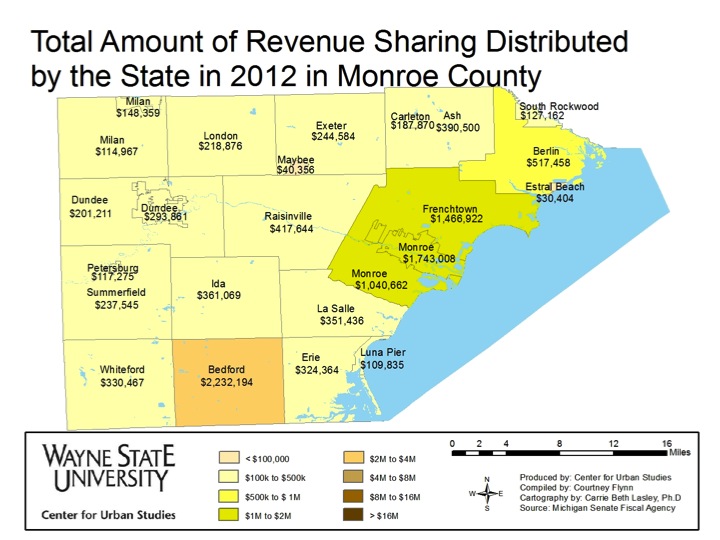

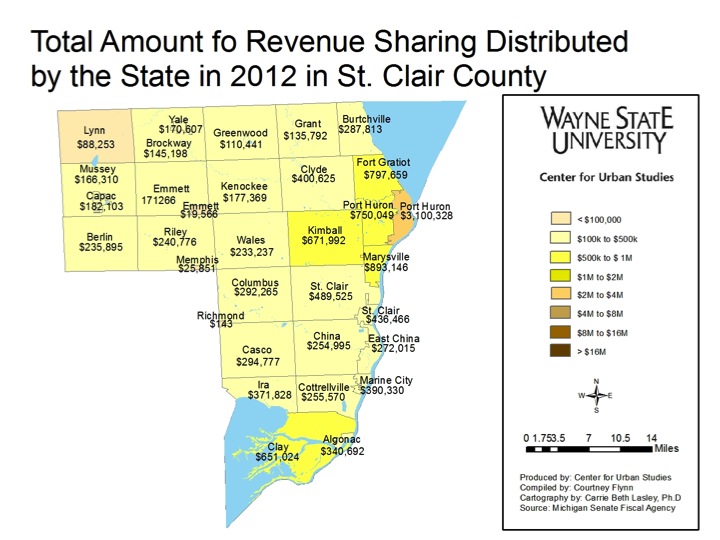

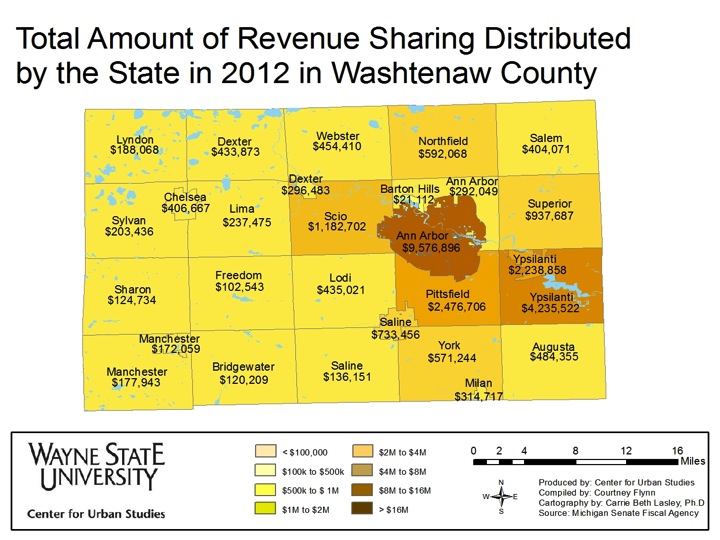

In the last post we examined how revenue sharing in Southeast Michigan has declined since 2003. In this post, the maps of each county show how much total revenue sharing each community in the seven-county region of Southeast Michigan received in 2012. Note that communities with higher populations (link to past population post), such as Detroit, received more funding.

The above maps show the total revenue sharing funds that municipalities in the seven-county region received in 2012. Detroit received the highest amount of funds at $175,532,461, according the Senate Fiscal Agency. Of all the municipalities in the region, Detroit also had the largest population; in 2013, it was estimated by the Southeast Council of Governments (SEMCOG) to have 681,090 residents.

There are 12 municipalities in the region that received less than a $100,000 in revenue sharing for 2012. Southfield Township in Oakland County received the lowest level of funding; it also had a population of 14,547, according to 2012 data from Munetrix; SEMCOG does not list Southfield Township. Estral Beach, a village in Monroe County, had the lowest population of all the municipalities in the region in 2012; according to SEMCOG it was 388.

As can be seen in the maps above, the counties with higher populations (Wayne, Oakland, and Macomb) received higher revenue sharing funding. This is because funding formulas are, in part, related to population.

According to the Michigan Department of Treasury, statutory /EVIP funds are distributed based on a formula. An upcoming post with provide examples of how these formulas have worked at different points in time. For now, it will help to know that the formula considers the following:

Population Unit Type – According to the Citizen’s Research Council (CRC), with the population unit type formula, cities are weighted the most and villages are weighted the least; to see how population and municipality type affect funding click here.

Taxable Value per Capita – The taxable value per capita formula takes the state’s average per capita taxable value and multiplies it by a given municipality’s population, according the Michigan Department of Treasury.

Yield Equalization – The yield equalization formula is used to “create a minimum guarantee on combined state and local revenue per mill of tax levy,” according to the CRC. This number is calculated by multiplying the number of mills in a local effort by the difference between the guaranteed and actual tax levy per capita; that number is then multiplied by the population in each municipality, according to the CRC.

Percent Share of Fiscal Year ’98 – According to the Michigan Department of Treasury, the percent share of fiscal year (FY) ’98 formula takes “each City, Village and Township’s FY ’98 statutory payments (Relative Tax Effort, Per Capita, and Inventory Reimbursement) and divides it by the FY ’98 Statewide Total Distributed to determine their Percent Share Factor.”

Beginning in 2002, 60 percent of the FY ’98 were paid using this formula; the percent paid then increased by 10 percent each year, according to the Michigan Department of Treasury.

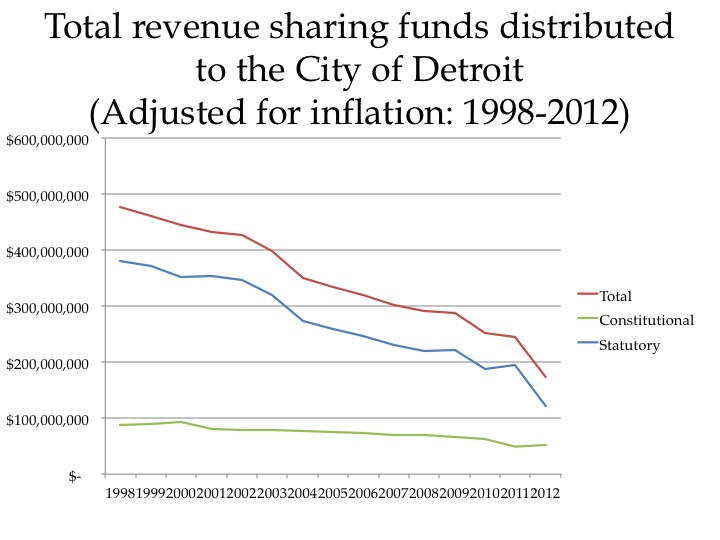

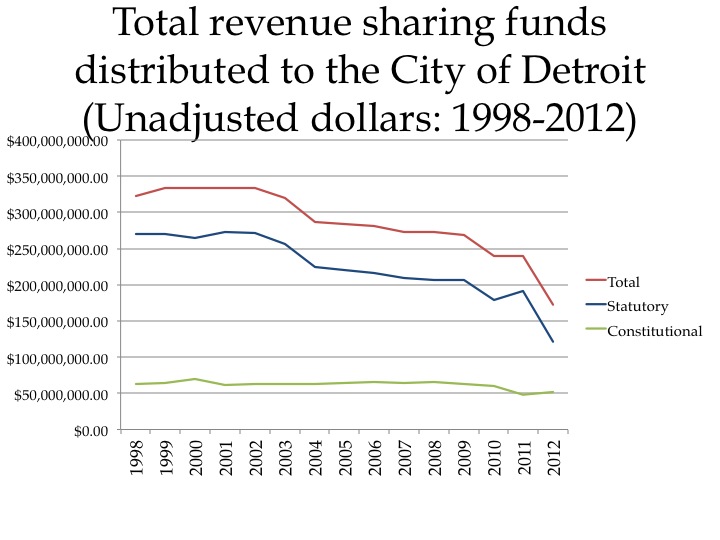

As we have seen in the last two posts, the amount of total revenue sharing funds distributed to municipalities across the Southeastern Michigan region has been decreasing, and Detroit is no exception. When looking at real dollars, the City of Detroit lost about $149.5 million in revenue sharing funding from 1998-2012; statutory funding represented about $148 million of that. Adjusting the number to account for inflation, using 1998 dollars as a base, Detroit lost about $304 million in total revenue sharing funding from 1998-2012, of which statutory funding represented approximately $255 million.

Up until 1998, the Relative Tax Effort (RTE), which was enacted in 1971, was intended to help monies follow communities’ needs, according to the CRC. However, there were complaints that cities fared better from the RTE than did townships and villages. This is why in 1998 an amendment was made to change how statutory funds were distributed. This amendment, which the formulas above reflect, shifted from distributing statutory funds based on intangibles, income, and small business taxes to providing 21.3% of sales tax revenues at the 4% tax rate, according to the CRC. Also, in 1998 then Gov. John Engler and Detroit Mayor Dennis Archer made a deal that the city would receive $333.9 million in annual revenue sharing funds if the city would decrease its city income tax rate, according to a Detroit Free Press Article and a Bridge Magazine report. Only a few years after the deal was made the state began to cut revenue sharing fund distributions, across the board. Since then Detroit has decreased its city income tax but has also not received the $333.9 million a year it was guaranteed.

In next week’s post we will provide examples of how the statutory revenue sharing formula has changed from 2002-2012 and how it has been beneficial to one community and detrimental to another.