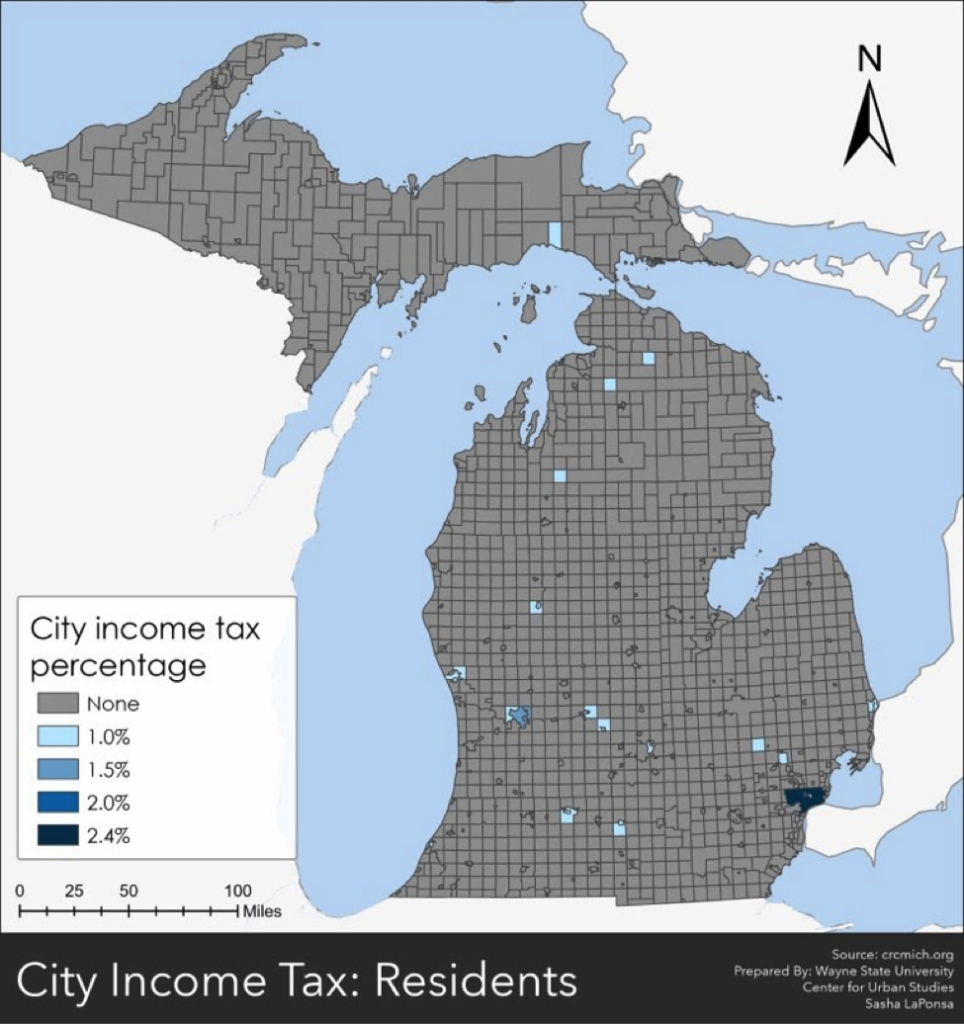

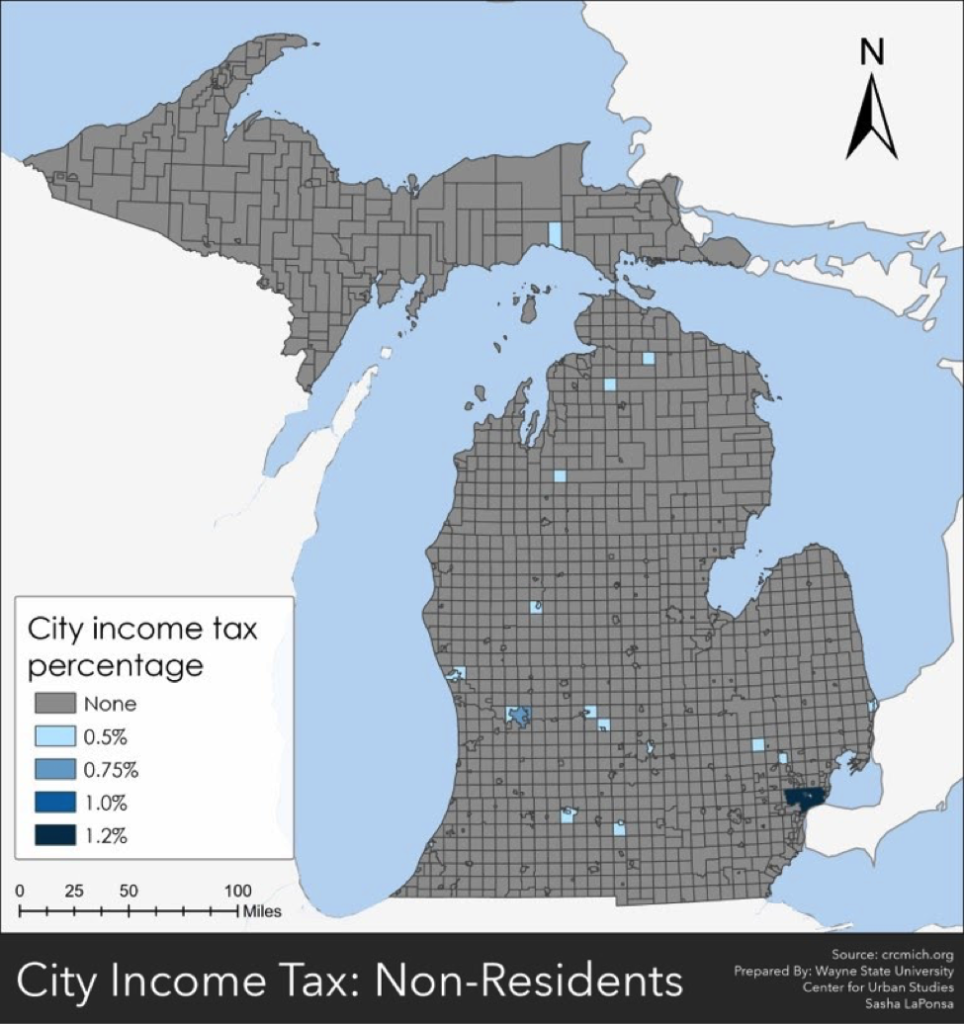

In the State of Michigan local governments have the ability to levy a local income tax on those who live and/or work in the municipality. There are 24 municipalities in Michigan that levy a local income tax for residents, non-residents and corporations. According to the Citizens Research Council of Michigan, the cities of Detroit and Hamtramck were the first two municipalities in the state to levy local income taxes in 1962. As of 2018 Detroit levied at 2.4 percent income tax on residents and a 1.2 percent income tax on non-residents. In Hamtramck, a 1 percent income tax was levied on residents and a 0.5 percent income tax was levied on non-residents. According to Michigan tax law, and as is shown, non-residents cannot be taxed more than 50 percent of the local income taxed on residents.

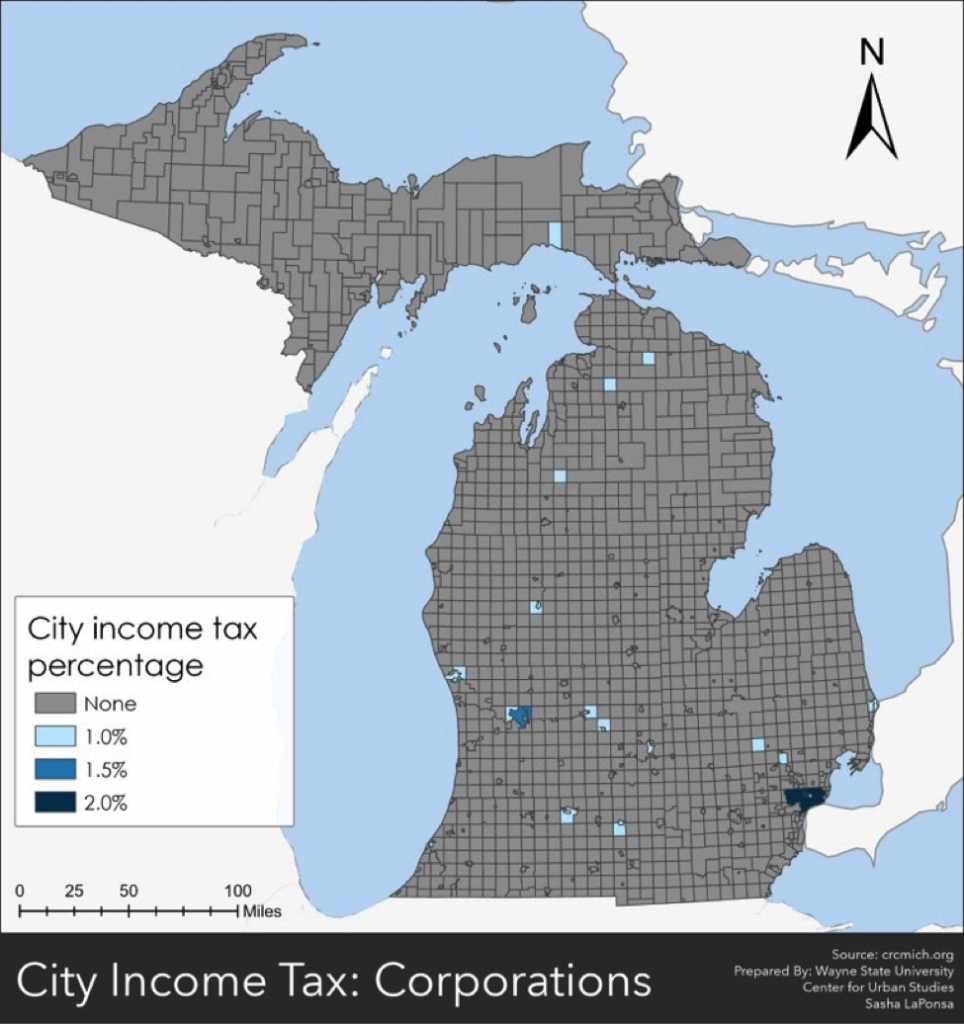

According to Michigan tax law, in general, a 1 percent income tax can be charged on residents and corporations and a 0.5 percent income tax can be changed to non-residents earned in the imposing city. The city council in cities over 600,000 (Detroit) may impose rates of up to 2.4 percent on residents, 2 percent on corporations and 1.2 on non-residents. Furthermore, a city that levied an income tax and where more than 22 mills had been levied for city purposes and at least 65 mills for all purposes during the prior calendar year is allowed to impose local income tax rates of up to 2 percent on residents and corporations and 1 percent on non-residents if approved by voters before Nov. 15, 1988. Additionally, cities that levied an income tax before March 30, 1989, and with (a) populations between 140,000 and 600,000 (Grand Rapids); or (b) populations between 65,000 and 100,000 in a county with a population below 300,000 (Saginaw) may increase the tax rate to not more than 1.5 percent on residents and corporations and 0.75 percent on nonresidents if approved by voters.

According to the State of Michigan, Detroit has the highest income tax at 2.4 percent, followed by the City of Highland Park at 2 percent (both of which are imposed on residents). A 2 percent local income tax was imposed on corporations in Detroit and Highland Park as recent as 2018, according to the Citizens Research Council.

In 2017 (most recent data available) Detroit levied about $292.7 million through its local income tax on residents, non-residents and corporations; Hamtramck levied $2.3 million Grand Rapids and Sagniaw each levied 1.5 percent income taxes on residents and corporations. Grand Rapids levied the second highest amount in local income taxes at about $94 million. Of course, the amount each city levies is not only dependent on the amount levied by the three groups but also by the population of who lives there, who works there and what businesses are there.

In addition to the cities above the, the following cities issue income taxes of 1 percent on residents and corporations:

- Albion

- Battle Creek

- Benton Harbor

- Big Rapids

- East Lansing

- Flint

- Grayling

- Hamtramck

- Hudson

- Ionia

- Jackson

- Lansing

- Lapeer

- Muskegon

- Muskegon Heights

- Pontiac

- Port Huron

- Portland

- Springfield

- Walker

The city that earned the lowest amount in a local income tax is Hudson at about $484,000.

In addition to the cities discussed above, the City of Mount Clemens has also discussed levying a local income tax to earn more local revenue. Mount Clemens is the county seat in Macomb County, which employs about 2,000 county employees. Local income taxes are a means for a local government to generate additional revenue. And, while it helps the local governments–especially ones who lack additional means to levy revenue–it also impacts those who live in the municipality and those who work and/or own a business there.